Universality is The Goal: Incremental Movement Toward Single Payer Options Makes Political Sense.

Posted on | September 1, 2017 | Comments Off on Universality is The Goal: Incremental Movement Toward Single Payer Options Makes Political Sense.

Mike Magee

As Trump continues to dabble in undermining the ACA, Democrats are pushing forward on an internal debate over the future of Obamacare. And although tactics and strategies are up for debate, there is close to a consensus on one issue – our government should guarantee universal health insurance coverage for all citizens. Our Code Blue campaign contains five core principles, listed below, that provide common ground in the debate.

The weaknesses of our current approach are now well-established including:

1. Not Universal: A CBO report predicting 27 million remaining uncovered by 2026.

2. Reporting Requirements: “Mind numbing” and time consuming requirements for documentation and reporting.

3. Administrative complexity: Robs time with patients.

4. Limited comprehensiveness: A trend toward “skinny plans” which are little better than no coverage at all. Physician and hospital panels are narrowing.

5. Underinsurance: A tripling of deductibles and “punishingly high copayments” paid by consumer.

6. Failure to Control Costs: ACA “has elicited ubiquitous gaming of risk adjustment and quality measure” incentives, spawning giant moves toward hospital and insurer consolidation.

7. Market-Based: “Any method of payment can create perverse incentives in a market-based system.”

The tension points in the internal debate were drawn into sharper relief when Sen. Brian Schatz (D-HI) released a new plan that would allow anyone in participating states to extend the opportunity to “buy-in” to their state Medicaid program. Essentially this would create open enrollment. According to Schatz’s vision, reimbursement rates for doctors and hospitals would rise to match Medicare rates insuring broad provider panels. Currently Medicaid reimburses at 72% of the rates of Medicare. Of course, states that passed on ACA Medicaid expansion (29 states under Republican governors) might pass on this offering as well.

The competing Democratic approach as outlined in a bill sponsored by Rep. John Conyers (D-MI) would go all-in on a national single-payer system. This has the virtue of actually achieving universal coverage since all individuals would be mandated to participate. The downsides include a predicted political firefight, massive disruption of the private insurance market (which would be relegated to providing supplemental insurance plans only – though back door involvement through plans mirroring Medicare Advantage might survive), and tax increases in the area of 10% likely to help finance the effort.

Schatz’s plan is not brand new. The Nevada legislature passed just such a plan this year, but Republican Gov. Brian Sandoval vetoed it. Way back in 1965, when Canada endorsed a single payer approach for all Canadians, Americans did the same – but only for those over 65. We called it Medicare, and while it has had issues over the past half century, Americans long ago decided they couldn’t live without it. Of course, until now, they also consented to widening income disparity and health inequality based on a system of “have’s” and “have-not’s” when it comes to the good fortune (or lack of the same) of possessing health insurance.

Medicaid expansion under the ACA celebrated a new approach (within the corridors of defined eligibility) of universality, access, health planning, portability, and integration with other social service programming. 18 of the 31 participating governors were Republican and liked the fact that the Obama expansion program was well funded, that the benefit package was broad (not a sham like the HSA induced high deductible/ empty benefit products proliferating everywhere), and that they preserved the flexibility within bounds to set the priorities on spending and defined how best to advance the overall health of their state populations. Add to this CHIP, a federal offering likely be extended, that provides coverage to economically needy children who find themselves slightly above poverty levels. In the wake of failed Repeal and Replace efforts, the remaining 19 hold-out Republican governors must now reconsider their ideologically driven stances. Some at least will reverse their stands.

The governors who have participated already have learned that centralized administration of a universally available health insurance offering carries distinct cost savings. Specifically, governor guided single payer health delivery under Medicaid came in 22% less costly than privately insured comparators. Governors like John Kasich of Ohio were left to wonder what might be the economic impact on Warren Buffett’s belief that health care was a “tapeworm on the American economy”. Analysts evaluation of single payer back office administration combined with state controlled and planned integrated health delivery shows a potential immediate 15% savings on our 4 trillion plus annual bill simply by consolidating management of coverage and payment systems.

Governors also could see that the human resource implications of such a move. Our purposefully complex program, which now threatens to break the American economy in much the same manner as reckless military spending collapsed the Soviet Union, has spawned 16 non-clinical jobs in health care for every one clinical role. A shift toward availability of single payer, if poorly planned and transitioned, could carry with it massive unemployment. But if you look at innovators like Kasich, what you see is the potential to reassign jobs by skill in a manner that could advance the strength of the social service network in areas like housing, nutrition, education, transportation and the environment.

Today’s Medicaid Numbers? 74 million or 20% of Americans currently covered; 11 million added under ACA; 40% of children covered; 50% of all births covered; 10 million disabled covered; 2/3rds of nursing home patients covered; 16% of health care spending nationwide; only 13% of citizens oppose Medicaid expansion.

Sen. Schatz recognizes a fundamental and permanent shift at work. He notes, “One of the unintended consequences of the Republicans trying to cut Medicaid is they made Medicaid really popular. This conversation has shifted. There was a time where Medicare was really popular and Medicaid was slightly less popular. What this ACA battle did was make both of them almost equally popular.”

The Code Blue Campaign endorses five core principles:

1. Universality: Health coverage and quality accessible health services are a right of citizenship in the United States.

2. Public Administration: Administration of basic health coverage is organized in the most cost-efficient manner possible with central oversight by the government. Incremental steps allowing the option of public sponsored plans to those already insured should be encouraged.

3. Local Control of Delivery: The actual delivery of services to ensure quality and cost effectiveness is provided by health professionals and hospitals at the local and state levels.

4. Health Planning is a Priority: Creating healthy populations is a high priority for each state governor. Working to establish health budgets and priorities, leaders must integrate health services with other social services, advance prevention planning and manage vulnerable populations.

5. Transparency: Providers submit bills. Government ensures payment of bills. Patients focus on wellness or recovery. Not all services will be covered. For uncovered services, those with the means to pay will be encouraged to purchase private supplemental insurance.

Tags: aca > Code Blue > Gov. Brian Sandoval > Gov. John Kasich > health reform > medicaid expansion > Obamacare > Rep. John Conyers > Sen. Brian Schatz > single payer

A Faustian Bargain Comes Home to Roost – Already!

Posted on | August 28, 2017 | 2 Comments

Valerie Huber

Mike Magee

“The Department of Health and Human Services is shaping up to be a huge headache for the radical Left”, crowed the Family Research Council in a June 12, 2017 release. Commenting specifically on the appointment of controversial nominee Valerie Huber, formerly head of the National Abstinence Education Association, as chief of staff for the Office of the Assistant Secretary for Health at HHS, it stated, “While conservatives cheered the move, the Left fired off a series of angry press releases, accusing Huber of being everything from anti-woman to anti-science. It’s almost comical…. The Left is so confused about basic biology that it doesn’t even know which bathroom to use!” “Congratulations, Secretary Tom Price, on another stellar pick!” Their words, not mine.

The appointment continued a Price/Trump trend begun in April, 2017, with the appointment of Charmaine Yoest, former president of Americans United for Life, as the Assistant Secretary of Public Affairs in HHS. She had worked earnestly to restrict access to abortion state by state, and along the way labeled transgender people “crazy”.

All of this is reminiscent of 2002. At the time, the new President Bush was knee deep in a tortured position on Stem Cell Research and the Pro-Choice/Pro-Life battle was in full swing. Candidates for service at HHS at that time had to make it through a phalanx of conservative evangelical organizations with names like Traditional Values Coalition, Family Research Council, Concerned Women for America, National Right To Life, U.S. Conference of Catholic Bishops, and of course Pat Robertson himself at the Christian Coalition.

The most controversial appointment surprisingly was Surgeon General. While the clearing venues varied, the temperature was consistent – somewhere between cold and frozen solid. In short, the very mention of the position of “Surgeon General” was a giant turn-off. The messages were clear and consistent. Number 1: We hate Koop because we supported him and he betrayed us. (C. Everett Koop MD, by then a decade out of service, had unleashed God-less AIDS education, advocacy and condoms on school children in their view.) Number 2: We’re never going to put ourselves in that position again.

If the message was clear, so were their preferences. Number 1: That the position of Surgeon General should be abolished or at least remain unfilled. Number 2: If it has to be filled, it must be filled by someone who would do absolutely nothing. Ceremonial only.

At the time, President Bush relied on a highly centralized White House personnel program to ensure the integrity of appointees to HHS. At the helm was one Ed Moy, Special Assistant to the President for Personnel. Ed was the only son of Chinese immigrants who settled in Wisconsin and established a successful Chinese-American restaurant there. He worked at the restaurant as a kid and attributed his strong focus on conservative economics to that experience. After dropping out of Pre-Med at the University of Wisconsin, he chose to double major in Economics and Political Science. At the same time, he met his future wife, Karen Johnson, a devout student interested in campus ministry.

Moy’s first job was as a salesman for managed care health policies at Blue Cross & Blue Shield of Wisconsin. During his ten year tenure there, he managed to become an ordained Christian minister and applied his skills to the benefit of students and faculty at his former alma mater. After working on Papa Bush’s campaign in 1988, he did a stint as the head of Managed Care for Health and Human Services in Washington. He returned to government service some years later when the second Bush gained the Presidency. His role this time, however, was as Special Assistant to the President for Personnel, a critical appointment to the self-proclaimed “born-again” George Bush who had anchored his campaign and owed his victory in part to the fierce loyalty of his supporters and to a pious pledge to support a new era of “compassionate conservatism”.

Control over personnel and messaging was designed to assure the right pedigree, values, and above all loyalty to George Bush. Under these conditions, evangelicals like Moy could be counted on to perform with “religous zeal” in assuring policy purity within the department.

When the AMA and AAMC offered a full-throated endorsement to Tom Price as Secretary of HHS, in return for a pledge of support of their parochial interests, they knew well this trade off. Some AMA Federation members like The American Congress of Obstetricians and Gynecologists (ACOG) hedged their bets. Here’s part of an ACOG’s letter to Price soon after his appointment: “Planned Parenthood clinics provide critical preventative healthcare services to women and men. Abortion is healthcare. ACOG remains committed to protecting each of these critical aspects of women’s health.” But those remarks were paired with these, “Your consistent efforts to find common ground and work together on shared goals are laudable, and your commitment to accomplishments, rather than talking points, is unfortunately all too rare in Washington. We hope that you will use your new role as an opportunity to expand on these collaborative practices.”

One need not be a genius to have predicted that in the age of Trump, this Faustian bargain would come home to roost in short order – yes, that Faust, “the magician and alchemist in German legend who sells his soul to the devil in exchange for power and knowledge.” So no surprise when the Trump administration this week abruptly announced the elimination of the final two years of funding for the Teen Pregnancy Prevention Program, a previously successful comprehensive federal effort that provides $89 million a year to 81 organizations. No matter that birth rates in teens, including minorities, are down significantly.

Bill Albert, spokesman at the National Campaign to Prevent Teen and Unplanned Pregnancy in Washington, D.C. sees the hands of Valerie Huber pulling the strings. “Maybe they don’t like the content of the program. They care more about telling kids to say ‘no’ rather than supporting programs that help teenagers.” Well known to Tom Price’s sponsors – in her position, Ms. Huber will directly impact the output of 12 public health offices including HIV/AIDS, Women’s Health, and Adolescent Health.

An early 16th century Faust play, often portrayed through puppetry, suggests a moment of truth:

“He laid the Holy Scriptures behind the door and under the bench, refused to be called doctor of Theology, but preferred to be styled doctor of Medicine.”

Tags: aamc > ACOG > ama > Donald Trump > Ed Moy > Faustian Bargain > HHS > medical leadership > organized medicine > Tom Price > valerie huber

Post-Charlottesville – We Need Caring Health Professionals More Than Ever!

Posted on | August 17, 2017 | Comments Off on Post-Charlottesville – We Need Caring Health Professionals More Than Ever!

Source: Jason Lappa, NYT

Source: Jason Lappa, NYT

Mike Magee

Collectively health professionals have a unique role in American society. Across cities and counties, rural and urban, we are asked to be available and accessible to help keep people well and respond when they are sick or injured. Those wounds come in all shapes and sizes – wounds to the body, wounds to the mind, wounds to the spirit. As important as are our diagnostic and therapeutic interventions to society, they pale in comparison to a larger, often over-looked function. Together, collectively, we process day to day, hour to hour, the fears and worries of our people, and in performing this function, create a more stable, more secure, more accepting and more loving nation.

With Charlottesville etched in the American psyche, good-willed Americans are in search of our true center. As a physician, I recall patients whose goodness and courage and kindness brought out the best in me and my colleagues. That after all is the true privilege and reward for doctors and nurses and all health professionals – the right to care.

Nearly six years ago, my wife and I were blessed with the arrival of our eighth and ninth grandchildren – two little girls, Charlotte and Luca. We were also introduced, for the first time as health consumers, to the Neonatal Intensive Care Unit (NICU). The girls came early, at 34 weeks, and struggled to work their way back up to their due date. They are doing great today, but in those early days, it wasn’t easy on them or their parents or the care teams committed to their well being.

Viewing them from my grandparent perch, the Connecticut Children’s Hospital Center NICU team at Hartford Hospital did a great job, balancing high tech with high touch, providing wisdom and reassurance, inclusion and training to the girls’ parents, who were inclusively inducted as part of the team on day one. Viewing it all from my vantage point as a former surgeon, hospital administrator and health policy analyst, I was impressed, but not surprised.

When people claim that “America has the best health care,” they’re usually referencing groups of highly skilled doctors and nurses and other caring professionals, committed to their patients and to each other, armed with experience, judgment and technology to – collectively – heal and provide health, and keep us whole in the process. It’s really a holy thing to observe.

What that NICU experience illustrates is that we health professionals are fully capable of collaborative and humanistic care, especially when faced with a complex crisis. But the challenge today, in the face of purposeful Presidential segregation of our citizenry, is to extend the same blend of knowledge, skill, compassion and partnership to all patients on a day-to-day basis. How do we assist them in creating healthy homes, healthy families and healthy communities?

If you deconstruct the success factors embedded in our NICU experience, what do you find, independent of the scientific skills, sophisticated technology and ultra-focus on the patient?

There are three elements that are worthy of note.

1. Inclusion: For most humans, the first instinct when faced with trauma or threat is flight. And yet, these NICU professionals’ first instinct was inclusion. With IVs running, and still groggy from her C-section, our daughter and her husband were wheeled to the NICU and introduced to their 3 lb. daughters. They were shown how to wash their hands carefully, how to hold the babies safely and without fear, and – while given no guarantees – experienced the transfer of confidence from the loving and capable caring professionals to them. Those were remarkable first day gifts to this young couple.

2. Knowledge: Coincident with the compassionate introduction to their daughters, there was a seamless transfer of information – each of their daughter’s current conditions, an explanation of the machines and their purposes, the potential threats that were being actively managed, and the likely chance of an excellent outcome. This knowledge – clear, concise, unvarnished, understandable – delivered softly, calmly, and compassionately, reinforced these young and fearful parents’ confidence and trust in each other, and in their care team, on whose performance their newborn daughters’ lives now depended.

3. Accessibility: Clearly a NICU is a 24/7 operation. But that alone did not assure that the needs of these patients and their family would be met. First, members of their care team needed to demonstrate “presence.” By this I mean, by communication, touch, voice, and face, they needed to connect to the parents, to signal that they cared for these unique individuals. The outreach needed to be “personal.” This was not a rote exercise for them, not just another set of parents, not just another set of tiny babies. These were these specific parents’ precious children, their lives, their futures were now in the balance. And the performance needed to be “professional.” The team needed to be consistent and collaborative, with systems and processes in place, no descent and little variability in performance, rapid response, anticipatory diagnostics and confident timely management of issues as they arose.

As we recover as a nation from Charlottesville and Trump’s self-inflicted wounds, we caring health professionals need to mirror a better way – holistic and inclusive, humanistic and scientific, where goodness and fairness reside side-by-side. How might each of us actively demonstrate a commitment to inclusion, knowledge transfer and accessibility, and in doing so, assure that our patients respond with confidence and trust in America?

“Let’s Make America Healthy Again!”

Posted on | August 8, 2017 | Comments Off on “Let’s Make America Healthy Again!”

Source: SSRS

Mike Magee

As the Democrats continue to angst over messaging and a platform to appeal to America’s middle class, the answer is staring them right in the face. A poll this week by SSRS made it abundantly clear. But before I go into that, let me provide a winning banner for the 2018 election: “Let’s Make America Healthy Again!”

The opinion polling on Trump above shows clearly that the President’s approval has broadly eroded over the past 200 days across the board. But nowhere is this more evident and more conclusive than in health care policy where 62% disapprove and only 31% remain in the Trumpcare corner. As interesting, but not surprising is the close runner-up and mirror for disapproval – “helping the middle-class”.

The economic case for moving progressively toward a universal, centrally administered/locally delivered system of health care has already been made by Warren Buffett and others. The potential savings are indisputable, and the gains in worker productivity, mobility, and family security could be transformational.

But if you were a governor of a state, let’s say like Ohio, how might you approach answering the question “How do I make Ohio healthy again?” Your first instinct might be to reactively throw all your resources at the raging opioid epidemic, but that would ignore a wide range of other priorities and opportunities.

You might take a moment to consider what you mean by health in the broadest terms rather than health care. If you were a seasoned leader, with strong ties to your community and public service flowing through your veins, you likely would conclude that health is an active state of wellbeing that encompasses mind, body and spirit. It is the capacity to reach one’s full human potential, and, on a larger scale, your own state’s potential for development.

As a governor, you might take the time to read the latest National Academy of Medicine publication “Building Sustainable Financing Structures for Population Health: Insights from Non-Health Sectors”, and highlight in yellow: “Health is often a side benefit of policy programs in other sectors”.

You would certainly want to take a moment to absorb one expert voice’s plea that “Many of the challenges that people face in the area of economic development and in realizing individual potential are health-related issues. For example, health care can be an invisible barrier to success in school performance.”

Having spent so much time in town meetings and walking the neighborhoods of your state, the words of another contributor would have to resonate: “The context in which people live affects health. There are numerous social determinants of health within one’s neighborhood – concentrated poverty, crime, walkable neighborhoods, the ability to exercise, access to healthy food.”

You would take a moment to reflect on the insight that the benfits of investments in the social determinants of health may not immediately ease a parent’s struggle but will change the trajectory of their children. “Have I considered a long enough horizon?”, you might ask yourself.

That horizon is effected not simply by the learning environment, nutrition and safety, but also by the physical environment. As the report declares, enlightened leaders “understand that everything they breathe at home and everything that comes through their pipes matters to their health.”

Finally, you would likely see in health, a broader call to action in the report’s words: “It is important to take a holistic look and realize that when making environmental changes, school changes, or economic changes, the capacity of the people in those communities must also be increased. They need to have or develop the agency, the voice, the leadership, and the capacity to govern their lives and become self-sufficient at a higher level because they are now living and working and trying to succeed in a new environment.”

Highlighting those final words, the governor – Republican or Democrat – might suddenly realize, “This is it – the unifying theme I’ve been searching for.” And standing to engage the next round of leaders who have just arrived at your state house doors, you might be overheard silently mumbling to yourself, “Let’s make America healthy again. I like the ring of that.”

Tags: “Building Sustainable Financing Structures for Population Health: > Health > health care > health policy > NAM > Social determinants of health

The Winning Argument For Universal Health Care Is Economic Not Ethical.

Posted on | August 3, 2017 | 2 Comments

(Check out your state HERE)

(Check out your state HERE)

Mike Magee

The optimistic top line headlines today dominated health news even while Congress struggles on the very basics of health delivery. “U.S. scientists fix disease genes in human embyos for the first time” blares USA Today. But turn to the Opinion page and you’ll find “Trump admits that sabotage is real Republican health care plan.”

What these competing headlines make clear once again is that scientific progress is not synonymous with human progress. Our faith in free enterprise and capitalism to “win the war” on disease (and supposedly leave “health” in its wake) dates back to the immediate post – WWII era. Over the years we’ve doubled down on this historically poor decision again and again, breeding profiteers, colluders, and promoters – but not much health for America.

The historic intermingling of health and business has yielded a long list of side-effects including: academic medicine’s rush for NIH grants, sellable patents, DTC advertising and AMA profiteering database sales, industry’s relentless assault on checks and balances and their expanding government relations, and government’s open door policy toward scientists with well known conflicts of interest. All spell success for the ever expanding Medical-Industrial Complex, but treat patients as pawns.

The cast of characters and drama that is unfolding resembles the Soviet Union’s demise on December 26, 1991. For a solid decade preceding this event, the power elite of that federation vigorously defended their status quo and the reckless build up of their military spending which eventually sent them over the financial cliff. Our misdirection of American healthcare is heading rapidly toward a similar endpoint.

The winning argument for a restructuring of our healthcare system and the movement toward single payers is economic not ethical. Universal coverage is necessary not because it’s a human right (which it is), but because risk must be shared to make insurance work, and uncovered citizens ultimately cost society more – much more! A healthy population is more productive, more likely to be educated, more mobile and willing to take risk, more likely to get married and have children, less likely to be involved in crime, violence, or injury. And all of this saves money.

When Warren Buffett said that “Medical costs are the tapeworm of American economic competitiveness”, he knew what he was talking about. But to responsibly transition ourselves out of this mess requires two things: 1) a vision/strategic plan, 2) the capacity to retrain and redirect health care workers from reactive health delivery to proactive and preventive social services.

On the vision front, studies clearly indicate that consolidating administrative back-office management of insurance sales, benefit management, and claims payments could immediately shave 15% off our national health care bill. But getting there is not as easy as uttering the magic phrase, “Medicare-for-all”. Let’s remind ourselves that while Medicare is quite efficient compared to private insurers, it is not a single-payer system. One third of Medicare enrollees voluntarily participate in Medicare Advantage plans run by private companies who receive special incentives and subsidies out of our tax dollars. The good news is that the government attaches strings to the deal like enforced caps on out-of-pocket expenses. Also one fourth of enrollees have supplemental “Medigap” policies.

Seniors strongly support Medicare as it exists, as do many employees who receive insurance as a work benefit. So when we begin to think about moving to a single payer, we need to think about an incremental option that allows those who wish to switch versus brute force. A huge change like this will take time, and flexibility is our friend not our enemy. For example, Canada leaves the planning, prioritization and delivery of care in their “single-payer” system in the hands of the separate provincial governments. This is not dissiliar to the way we expanded Medicaid, providing baseline standards and financial subsidies from the federal government but giving each governor the authority to balance and integrate local health delivery with a range of other social services. Having local control of both buckets may be essential in transitioning workers in the near future.

Workforce transition is at least as great a challenge as shared responsibility. For every one physician in America, there are 16 additional health care workers. Approximately half of them are non-clinicians uninvolved in hands-on care. And not all the clinicians actually care for patients either. Name brand doctors in big academic centers today, touting “personalized medicine” this and “personalized health” that often more closely resemble dot-com entrepreneurs than the hands-on caregivers making rounds and teaching house staff of years gone by.

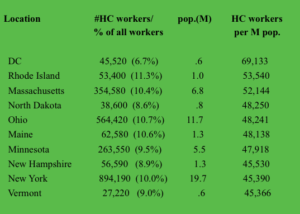

Health care now includes 11% of all workers compared to 8% in 2000. Since the country’s near financial collapse in 2007, 35% of the job growth has been in health care, fueled by aging demographics and the expansion of Medicaid under the ACA. More than 1/2 of the nearly $4 trillion spent on health care in the U.S. goes to wages. You can find a list of some the jobs, along with average salary and educational requirements HERE. The American Academy of Professional Coders is now nearly 200,000 strong with average salary approaching $50,000 a year. Near 20% growth in healthcare jobs is projected by the government in the coming decade, adding an additional 2.3 million positions is we maintain the status quo.

Shifting toward universality, planning, prevention, and efficient management will be profoundly disruptive to many workers. The impact would vary from state to state depending on their historic over-weighting of the health care sector. For example, listed above are the top ten states (including D.C.) ranked by the highest number of health sector workers (excluding those self-employed) per million citizens. The D.C. outlier reflects the Medical-Industrial Complex’s commitment to self-interest lobbying. States like Massachusetts, Rhode Island and New York have large academic enterprises with active industry partners. States like North Dakota, Maine, New Hampshire and Vermont have small widespread rural populations many of whom are economically vulnerable.

The point is, adjustments of work force in response to substantitive health care reform would need to be addressed on the local level and would be a significant challenge to state governors.

A starting point would be to deconstruct enterprises which primarily service direct care needs from those engaged in speculative scientific discovery for profit. These are radically different entities. Step two would be to integrate direct patient care with the continuum of social services. Plan for health, not disease. Finally, be bold. If we want to avoid Russia’s fate, change must be our friend.

Tags: health and economics > health care crisis > health care workers > health care workforce > healthcare reform > medical-industrial complex > single payer > warren buffett

How Medicaid Is Socializing and Polularizing Single Payer Approaches To Population Health.

Posted on | July 25, 2017 | 2 Comments

Mike Magee

As the Republican controlled Senate prepares for a ballot today to vote on a bill yet to be identified, their governor counterparts in 31 of our 50 states are fast at work familiarizing themselves and socializing themselves to a new way of managing the health of populations within their geographic boundaries – single payer systems.

Despite the attempt to brand the term “single payer” the way that Medicare was attacked a half century ago as big government “socialized medicine”, the majority of governors has tacitly acknowledged what Warren Buffett described as a health care status quo that is “the tapeworm of American economic competitiveness”. The decline of state economies reinforced by the burden of weak social systems, challenged and undermined by a raging opioid epidemic, have caused Republican governors like John Kasich to declare independence when it comes to health policy.

Way back in 1965, when Canada endorsed a single payer approach for all Canadians, Americans did the same – but only for those over 65. We called it Medicare, and while it has had issues over the past half century, Americans long ago decided they couldn’t live without it. Of course, until now, they also consented to widening income disparity and health inequality based on a system of “have’s” and “have-not’s” when it comes to the good fortune (or lack of the same) of possessing health insurance.

President Obama’s federal subsidization of an expanded Medicaid with broader eligibilty and more generous coverage and protections hit the sweet spot with all but the reddest of red state governors. Those hold-out’s were literally willing to financially cut off their noses to spite their faces. For others like Kasich who were willing to give President Obama a chance, they liked the way it felt to actually lead and so did the citizens in their communities.

Medicaid celebrated a new approach (within the corridors of defined eligibily) of universality, access, health planning, portability, and integration with other social service programming. Participating governors liked the fact that the program was well funded, that the benefit package was broad (not a sham like the HSA induced high deductible/ empty benefit products proliferating everywhere), and that they preserved the flexibility within bounds to set the priorities on spending and defined how best to advance the overall health of their state populations.

The governors learned that centralized administration of a universally available health insurance offering carried distinct cost savings. Specifically, governor guided single payer health delivery under Medicaid came in 22% less costly than privately insured comparators. Governors like Kasich were left to wonder what might be the economic impact on Buffett’s “tapeworm” were their lessons to be applied across our entire population – single payer back office administration combined with state controlled and planned integrated health delivery. They read the studies that showed a potential immediate 15% savings on our 4 trillion plus annual bill simply by consolidating management of a universal coverage approach in a central systematized fashion.

Governors also could see that the human resource implications of such a move. Our purposefully complex program, which now threatens to break the American economy in much the same manner as reckless military spending collapsed the Soviet Union, has spawned 16 non-clinical jobs in health care for every one clinical role. A shift to single payer, poorly planned and transitioned, could carry with it massive unemployment. But if you look at innovators like Kasich, what you see is active reassignment of jobs by skill in a manner that advances the public good. The governor well understands that the U.S. is the only civilized nation in the world where more is spent on the mechanics of disease fighting than on all social services combined – the very combination of services and supports that help keep a population well. With flexibility, as wildly expensive nursing home use declines, those employees, now mobile, are an immediately useful and experienced mobile home services health corps. Given room for innovation, as they have been under the ACA, governors have applied both innovation and structural remodeling to expand safety, security, and health across multi-generational families.

The Medicaid single payer experiment has been large scale. Under the direction of autonomous state leaders, 77 million have received care of late with extraordinary high satisfaction levels. 34 million of these citizens are children. 2 million new citizens will be ushered into the human race this year through Medicaid prenatal and obstetric coverage. 9 million blind and disabled citizens sleep easier each night thanks to the governors. By 2026, absent Trumpcare regression, the 77 million will grow to 86 million with 35 million children in the ranks. Nearly a third of the states structure offerings through a managed care approach. All integrate physical and mental health, including addiction services.

Governors like Kasich have turned a critical eye toward waste. For example, Medicaid has historically been the primary payer of long term care – specifically nursing homes. Over decades, perverse incentives have created a lawyer and nursing home industry driven cottage industry designed to divest seniors of their assets so that they could reach eligibility requirements to have free nursing home care. Nearly half of all spending for long term care in the US – over $150 billion a year – comes from Medicaid. Flexibility provided to governors like Kasich could allow the realignment of financial incentives with funds provided for home services to multi-generational families who do right by their seniors rather than abandon or warehouse them.

Innovative programs like Money Follows the Person or The Program of All-Inclusive Care for the Elderly (PACE) should not be confused with the Senate Republicans offerings. Their caps have little if anything to do with innovation and more to do with transferring some $800 billion over the next 10 years from the neediest to the wealthiest Americans in the form of tax cuts.

Trump and his followers may be intent on creating chaos, promoting regressive legislation, and reimagining reality, but governors in most states are laser focused on solutions – and the more they experience single payer efficiency, control, and integrated health planning, the more they and their citizens like it.

Tags: aca > John Kasich > Medicaid > Obamacare > Senate Republicans > Trumpcare

Doctor Senators Barrasso and Price – They Are No Royal Copeland.

Posted on | July 14, 2017 | 1 Comment

Sen. Royal Copeland M.D. (D, NY)

Mike Magee

This week the Republican leadership once again released an unapologetically regressive plan for America’s healthcare that would drive a further wedge between rich and poor and sow despair deep into America’s soul. Sadly, two of the primary leaders of the effort are fellow physicians, Sen. John Barrasso (R,WY) and former Sen. Tom Price (R, GA). This in the same week that we learn that America’s childhood go-to staple, Kraft boxed Mac & Cheese, has been laced with endocrine disrupting phthalates all along and no one seems to have noticed.

Barrasso and Price stand in steep contrast to other historic physician legislators. For example, in 1932, with FDR fully in charge and the New Deal gaining momentum, Walter Campbell, the director of the FDA, and the Assistant Secretary of Agriculture, Rexford Tugwell, put a proposal in front of FDR to strengthen the enforcement powers of the 1906 FDA law. Their ally in Congress was a physician and former New York City Commissioner of Health, now senator from New York, Royal S. Copeland M.D..

Copeland gave it his all, but it was an exercise in futility. To begin with, he was opposed by a wide range of interests from food to drug manufacturers to cosmetic makers. But more importantly, the newspaper and magazine publishers viewed “over-regulation” of this free wielding American sector as an existential threat to them. After all, the advertising dollars spent by every Tom, Dick and Harry with a “miracle cure” were considerable. And that was without counting the food manufacturers whose wallets were wide open as they worked to establish their various national brands. To these publishers, tighter health controls meant tighter marketing budgets. To make matters worse, the Copeland supported legislation would involve itself in regulating the murky area of “false advertising”, and “who knows where that could end”.

But the truth is that at the time the various commercial interests were not too worried about the FDA’s Walter Campbell, or his boss in Agriculture, Rexford Tugwell, or even the Senate’s Royal Copeland. Health legislation was low on the list of priorities in FDR’s New Deal. It was going nowhere fast – that is, until October 11, 1937. That was the day that the American Medical Association was informed by one of its physicians that a number of children in Tulsa, Oklahoma had taken a new sulfanilamide liquid medicine and died.

AMA labs quickly identified the killing agent as diethylene glycol used as a mixing agent in the elixir of sulfanilamide produced by S.E. Massengill and Co. in Bristol, Tennessee. The mix had passed the taste test of the company’s chief chemist, but he had somehow missed that diethylene glycol was a known poison used in anti-freeze. At the time, no safety tests were required before release of medicines on our citizenry.

“Elixir Sulfanilamide” was rushed into production and distributed widely. 240 gallons of the red liquid made it’s way to 31 states, through a web-like network with many small distributors. That was in early September, 1937. In all, over the next 6 weeks 100 children died. And their deaths were not simple. They were proceeded by 7 to 21 days of wrenching painful illness including “stoppage of urine, severe abdominal pain, nausea, vomiting, stupor, and convulsions”.

One young mother spoke for everyone affected in her 1937 letter to FDR:

“The first time I ever had occasion to call in a doctor for [Joan] and she was given Elixir of Sulfanilamide. All that is left to us is the caring for her little grave. Even the memory of her is mixed with sorrow for we can see her little body tossing to and fro and hear that little voice screaming with pain and it seems as though it would drive me insane. … It is my plea that you will take steps to prevent such sales of drugs that will take little lives and leave such suffering behind and such a bleak outlook on the future as I have tonight.”

Doctors, in a manner reminiscent of contemporary physicians who carelessly over-prescribed Oxycontin and ignited the current Opioid Epidemic, were remorseful as well. Consider Dr. Archie Calhoun, of Mount Olive, Mississippi, who wrote on October 22, 1937:

“Nobody but Almighty God and I can know what I have been through these past few days. I have been familiar with death in the years since I received my M.D. from Tulane University School of Medicine with the rest of my class of 1911. Covington County has been my home. I have practiced here for years. Any doctor who has practiced more than a quarter of a century has seen his share of death. But to realize that six human beings, all of them my patients, one of them my best friend, are dead because they took medicine that I prescribed for them innocently, and to realize that that medicine which I had used for years in such cases suddenly had become a deadly poison in its newest and most modern form, as recommended by a great and reputable pharmaceutical firm in Tennessee: well, that realization has given me such days and nights of mental and spiritual agony as I did not believe a human being could undergo and survive. I have known hours when death for me would be a welcome relief from this agony.”

The whole disaster was vigorously reported in the press, including the powerful New York media, home state of FDR, Chief Justice Hughes and Royal Copeland. It was a New York physician, learning of the AMA’s involvement on October 14, 1937, who first had contacted Walter Campbell at the FDA and got the policy ball rolling. As a result of the tragedy, the issue was now a New Deal priority and on everyone’s radar screen. Copeland and Campbell teamed up on legislation.

The AMA, the American Pharmaceutical Association, women’s groups and the national press all closed ranks in support. It didn’t hurt that the main Congressional opponent of Royal Copeland’s legislation was Representative Carroll Reece from Tennessee, home state of the S.E. Massengill Company. Copeland harnessed the power of the media writing an impassioned editorial in Scientific American where he detailed the deficiencies of the 1906 law.

On November 16, 1937, Senator Copeland formally addressed the tragedy on the Senate floor and asked the Department of Agriculture, which had jurisdiction over the FDA, to issue a formal investigative report on the tragedy. Over the next six months he worked tirelessly on corrective legislation. By June 11, 1938, bills from the Senate and House of Representatives had been reconciled, and on June 25, 1938, FDR signed into law the 1938 Federal Food, Drug, and Cosmetic Act.

Tags: Elixir Sulfanilamide > FDA > fda law > FDR > John Barrasso > Massengill Tragedy > Phthalates in Mac and Cheese > Republican Health Carre > Senator Royal Cpeland > Tom Price > Trumpcare

"Code Blue INDEX online"

![]()

![]()

Prospective Health Blog

BIOGRAPHY

Homegrown Friends

BIOGRAPHY

NIH Precision Medicine

BIOGRAPHY

Health in 30

BIOGRAPHY

Larry's Letters

BIOGRAPHY

Precision Medicine, Euthanasia, Abortion, Communism, Trillions of Dollars, Losing Freedom, and Town Hall Mobs BIOGRAPHY

Yearning for Universal Coverage Is Not Universal

BIOGRAPHY